Making a VA Home purchase easy with Ed Kinkopf

U.S. Military on the Move® (MOM) is a real estate program offered by top independent real estate companies who are experts in their local markets, created as a special thanks to those who have served in the military. If you are buying or selling a home, our agents have the experience and reputation to deliver superior real estate service and special rewards.

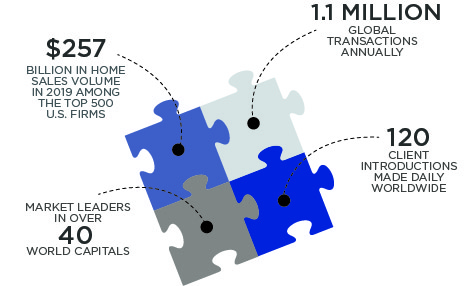

The network behind U.S. Military on the Move®

VA Mortgages: The “Thank You for Your Service” Home Loan

By Susan Doktor

Home financing options abound—to the point where many homebuyers struggle to understand the differences among them. Finding the mortgage solution that’s best suited to your needs can be a challenge. But if you’re a veteran, an active military service member, or a military spouse, often the smartest, most economical choice is a Veterans Administration (VA) loan. VA loans, which are insured by the federal government, were designed to put homeownership within easier reach for service members (and their families) who put their lives on the line to protect our country.

Why Consider a VA Mortgage for Your Manatee County Home?

Soldiers provide an incalculably valuable service. Most people would agree, though, that the pay they earn doesn’t equal what they contribute or sacrifice to protect our country. In 2021, the average salary of a US Army member was about $30,000 per year. Needless to say no one is living the life of luxury on a soldier’s pay. And VA loans are one way that the government tries to even the score. These mortgages offer benefits no other type of loan can match. Let’s take a look at some of the features that make VA loans so exceptional.

Easier Eligibility For Veteran Homebuyers

There’s nothing more frustrating for a homebuyer than being turned down by lender after lender for not meeting the wide range of loan qualifications required to secure a mortgage. Typically, these qualifications include having a credit score in the mid-600s at least, being able to make a sizeable down payment, and purchasing a home that offers a low loan-to-value ratio. Each of these eligibility criteria may be more lenient with a VA loan.

The Gift That Keeps on Giving

Your VA mortgage benefits last a lifetime. You can apply for a VA loan as many times as you wish. If you previously purchased a home with another type of mortgage, you can refinance it into a more advantageous VA loan any time, so long as it’s your primary residence. You can also access the equity you’ve built up in your home by doing a cash-out refinance. You can borrow more than you currently owe on your home, receive the proceeds at closing, and use the funds for important expenses like college tuition for your kids or major home improvement projects that can further increase your home’s value. In some cases, you can even take out a loan for 100% of your home’s value—that’s not true of most conventional loans.

Tax Advantages of Homeownership

Owning a home is not only a closely-held dream for many Americans, it’s also a way to make your money work harder for you. When you pay rent, you have nothing to show for it at the end of the month. When you pay your mortgage, you build a financial nest-egg in your home, also known as home equity. Come April 15th each year, homeowners also enjoy a tax advantage, by way of the mortgage interest tax deduction. In other words, you can deduct the amount of mortgage interest you pay each year from the income your tax is figured on. Less income, less tax.

No Down Payment? No Worries!

Conventional mortgage lenders require you to put some significant skin in the game before they’ll give you a loan. Young homebuyers, particularly those who serve in the military, may not have had the time to save up for a sizable down payment. VA loans are often available with no down payment whatsoever. That’ s probably their single greatest advantage and how they helped 1.2 million military personnel join the ranks of happy homeowners.

Military Service Members Can Avoid the PMI Pitfall

You may be able to find a lender who’ll give you a mortgage if you make a low down payment on your home. But typically you’d have to pay something called private mortgage insurance (PMI) until you have built up sufficient equity in your home—usually about 20% of the value of your home. Private mortgage insurance generally costs between 0.5% and 1.0% of the amount of your outstanding mortgage balance. If you owe $100,000 on your home, that means you’d wind up spending between $500 and $1000 per year on PMI each year. Wouldn’t you rather sock that money in the bank or put it towards your kids’ college tuition? Well, with a VA loan, you can. You’ll never have to pay PMI on a VA mortgage.

Pay Less Interest, Keep More of Your Money

Lenders normally reserve their best interest rates for their most qualified borrowers. The rates you see advertised on bank and mortgage marketplace websites are the lowest rates offered, not the rates every borrower will get. VA loan interest rates are consistently lower than traditional mortgage interest rates, despite having more favorable features than conventional mortgages. That means both your monthly payments and the lifetime cost of owning your home will be lower.

How Much Can I Borrow in Manatee and Sarasota Counties with a VA Loan?

The current standard VA loan limit is $548,250. That buys a pretty impressive home in both Manatee and Sarasota Counties. However, depending on where your new home is located, you may be able to borrow considerably more. The VA recognizes that some zip codes are just more costly than others. But homebuyers should understand that they may not be able to borrow up to the limit. How much a lender will lend you depends on many factors, including whether you’re paying a realistic price for your home and your debt-to-income-ratio. Lenders want to be assured of two things: the first is that they are making a sound investment and the second is that you will be able to afford your monthly mortgage, insurance, and property tax payments.

How to Find a VA Loan

While VA mortgages are backed by the federal government, the government doesn’t actually loan you the money to buy your house. To apply for a VA mortgage, you must work with a bank or other lending institution. Many, but not all lenders offer VA loans. In addition, the government doesn’t set mortgage interest rates or all eligibility requirements for VA loans. These will vary by lender. While VA mortgages are unique among home financing solutions, they’re like every other kind of loan in one way: it pays to shop around for the best deal. You can rely on your Manatee County realtor to point you in the direction of licensed VA mortgage lenders who are committed to treating veterans right.

Author Bio:

Susan Doktor is a journalist, business strategist, and principal at Branddoktor. She writes on a wide range of topics, including finance, real estate, and government affairs. Follow her on Twitter @branddoktor.

Privacy Policy / DMCA Notice / ADA Accessibility